Key takeaways

- Altcoins aren’t built for daily use. Volatility keeps Bitcoin and others out of future checkout lines.

- Stablecoins dominate today’s digital infrastructure – fast, fiat-pegged, and already handling most crypto transaction value.

- CBDCs are the state-backed answer – legal tender designed to protect monetary sovereignty, tax compliance, and stability.

- Coexistence is likely, but CBDCs lead at the register. CBDCs are the natural resolution in the future of digital payments.

Here’s the simple picture – Bitcoin and most altcoins aren’t built for everyday spending.

Prices swing too much to set groceries or payroll. Even in a calmer year, BTC’s 30-day realized volatility often sits in the 25-40% range, and real-world pilots haven’t shown broad checkout use (in El Salvador, about 88% of people didn’t use Bitcoin for transactions in 2023).

Stablecoins work better for daily payments today. They’re fiat-pegged, fast, and already moving trillions across networks, with Visa and others wiring them into familiar payment flows.

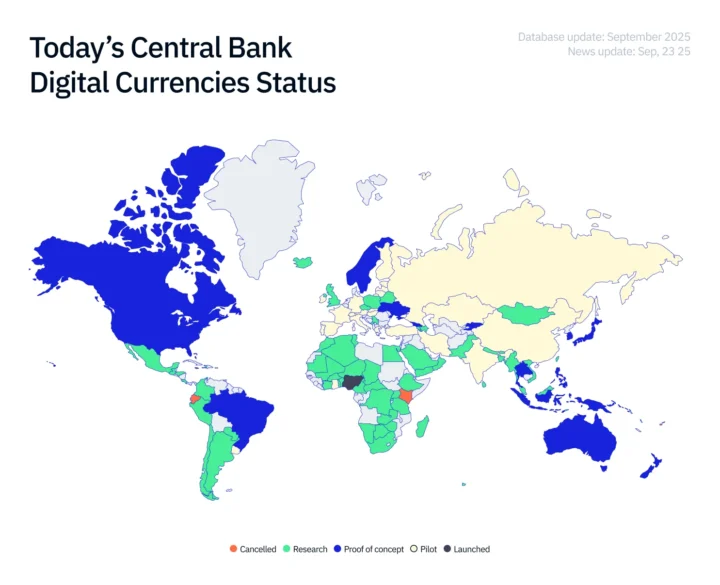

CBDCs (Central bank digital currencies) are the next step. Central banks want digital cash that’s legal tender, widely accepted, and under public oversight. As a matter of fact, 91% of surveyed central banks were exploring a CBDC by 2024.

This article follows that latter prediction. How can we be so sure that stablecoin dominance is a precursor to a CBDC-led global economy?

Understanding Stablecoins and CBDCs

Stablecoins are crypto tokens designed to hold a steady price, usually by pegging to fiat (most often the U.S. dollar). Issued by private companies, they’re backed by reserves (cash, T-bills, or similar assets) and redeemed 1:1 with the issuer.

Names like USDT and USDC dominate because they’re fast, easy to integrate, and highly interoperable (handy for cross-border payments, remittances, and moving value between platforms without touching traditional infrastructure).

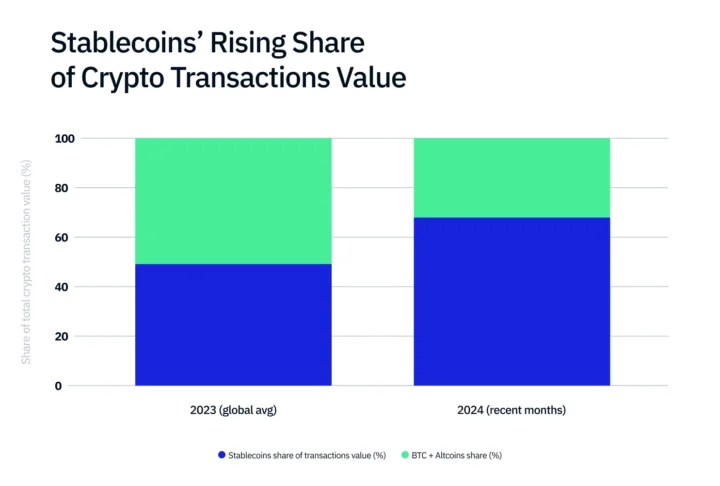

Stablecoins have already started to dominate crypto transactions, overtaking BTC and altcoins as the primary infrastructure for digital value transfer.

CBDCs are different: they’re official digital cash, a direct claim on the central bank (legal tender by design). A retail CBDC targets everyday daily payments; a wholesale one serves banks and market infrastructure.

Examples include China’s e-CNY, the proposed digital euro, and ongoing debates around a US digital dollar / Fed CBDC. Design can be centralized or permissioned, but the goals are similar: efficiency, tax compliance, resilience, and monetary sovereignty.

So, in a CBDC vs stablecoin debate, the core difference is who guarantees the value (state vs private issuer) and how the system is governed.

Here’s Why CBDCs Will Replace Stablecoins

As crypto adoption accelerates, governments are keen to head off potential crises. It’s increasingly likely they’ll aim to shift stablecoin use toward their own CBDCs – and here’s why.

To keep monetary control

Policymakers worry that if everyday money shifts to private stablecoins, deposits drain from banks, credit creation shrinks, and monetary policy loses bite. Academic and policy analysis flags this risk directly: stablecoin adoption can weaken central banks’ control and undermine bank funding. That’s a core tension in the CBDC vs stablecoin debate.

To protect the tax base and fight illicit finance

Moving value over opaque private rails makes tax compliance and AML harder. One widely cited estimate suggests only 0.53% of crypto investors paid taxes in 2022 – methodology debated, but the signal is clear enough for regulators. Retail CBDC designs often explore “managed anonymity”: small-value privacy with traceability at higher thresholds, aiming to balance privacy with enforceability.

To preserve monetary sovereignty

Heavy use of foreign or privately issued tokens for daily payments can erode demand for the local unit of account. China’s e-CNY sits alongside a strict stance on private crypto – an approach tied to sovereignty, capital controls, and oversight of payment data. Europe’s digital euro work and U.S. Fed CBDC debates reflect similar sovereignty concerns, even if designs differ.

To follow the momentum

Central bank exploration is now the norm. The BIS reported 91% of 93 central banks were working on CBDCs in 2024; global trackers show the majority of economies (by country count and share of GDP) are in research, development, or pilot, with a record number of live pilots. In short, if money is going digital, public money will too.

This is the policy backdrop for the CBDC vs stablecoins difference: CBDCs promise legal-tender finality and standardized oversight for point-of-sale, cross-border payments, and remittances; stablecoins bring private-sector speed and interoperability, but raise questions about stablecoin regulation, reserve backing, and who ultimately governs the rails.

The Case for Stablecoins

There’s also a counterargument: the continued dominance of stablecoins, operating alongside and integrated with traditional financial infrastructure.

Why fix something that’s not broken?

Stablecoins already move value quickly across borders, settle 24/7, and slot into existing crypto systems for trading, remittances, and cross-border payments. In countries with shaky currencies, dollar-pegged stablecoins have become a practical store of value – what CGD calls “digital dollarization,” as households and businesses lean on USD-linked tokens when local money erodes.

The private sector is meeting users where they are

Visa is building out stablecoin settlement and stablecoin-linked cards, positioning them for retail merchant acceptance across its network. Mastercard has announced end-to-end capabilities “from wallets to checkouts,” signaling that stablecoins aren’t just for crypto exchanges but for mainstream payouts and commerce.

These moves don’t make every checkout “crypto-ready” overnight, but they do lower the integration hurdle for wallets and fintechs that want tap-to-pay with a stablecoin balance.

Big merchants are kicking the tires

The ECB notes that major card schemes are integrating stablecoins and that U.S. giants like Walmart and Amazon are exploring their use – an early sign that stablecoins could surface inside familiar shopping flows rather than niche apps.

Privacy and choice also matter in the CBDC vs stablecoin debate. A central bank digital currency can raise CBDC privacy concerns because it’s state money by design; a privately issued stablecoin can feel less like a government view into every transaction. That doesn’t make stablecoins anonymous (issuers face stablecoin regulation and compliance), but for users uneasy about pervasive monitoring, having a private-issuer option is meaningful.

Policy (in some markets) tilts toward regulated stablecoins over a retail CBDC

In the United States, Congress has advanced stablecoin legislation (e.g., the GENIUS Act) while anti-CBDC measures gained traction, and a 2025 executive order directed agencies not to pursue a U.S. retail CBDC. In this environment, regulated dollar stablecoins may carry the “digital dollar” forward without a Fed CBDC, at least for now.

CBDCs vs. Stablecoins – Side-by-Side

| CBDCs | Stablecoins | |

| Who issues it | Central banks (e.g., digital euro, e-CNY) | Private companies (e.g., USDT, USDC) |

| Legal status | Legal tender, backed by the state | Private tokens rely on reserve backing and regulation |

| Trust | Guaranteed by the government | Trust depends on issuer transparency and audits |

| Privacy | Raises CBDC privacy and surveillance concerns | Pseudonymous, but issuers still follow KYC/AML |

| Main uses | Everyday domestic payments, government transfers, and interbank settlement (wholesale CBDC) | Cross-border payments, remittances, crypto trading, and early merchant trials |

| Current status | 91% of central banks exploring; pilots live in China and Europe | Already dominate crypto flows, making up over two-thirds of transaction value |

| Key risks | Bank disintermediation, slower rollout, political debate | De-pegging, uneven regulation, and reliance on private firms |

CBDC Dominance Is Inevitable

Both stablecoins and central bank digital currency will shape digital money, but for routine daily payments and point-of-sale, the edge likely goes to retail CBDC: it’s legal tender, anchors monetary sovereignty, and gives governments the levers they need for tax compliance and stability.

Surveys show the policy direction is clear (most central banks are actively pursuing CBDCs) and large jurisdictions are testing real programs like e-CNY and the digital euro.

Stablecoins won’t vanish quickly. They already excel at cross-border payments and remittances, and private networks are wiring them into mainstream payment systems (from Visa’s stablecoin settlement to Mastercard’s “wallets-to-checkouts” stack), supporting broader merchant acceptance under clearer rules (e.g., MiCA stablecoins) and stronger reserve backing.

Still, the CBDC vs stablecoins difference (state money vs privately issued tokens) will guide who leads at the register. In the U.S., skepticism of a Fed CBDC leaves space for regulated dollar stablecoins; elsewhere, public money is moving first.

FAQ – Stablecoins vs. CBDCs

1) What’s the CBDC vs stablecoin difference in plain terms?

A central bank digital currency (CBDC) is public money, a legal tender, and a direct claim on a central bank. A stablecoin is private money – tokens backed by issuer reserves (cash, T-bills, etc.) under varying stablecoin regulation. In short: state-issued and policy-anchored vs privately issued and market-governed.

2) Which is better for daily payments and point-of-sale?

For daily payments and merchant acceptance, a retail CBDC offers legal-tender finality and standardized tax compliance. Stablecoins already work well, especially in wallets and apps, but their acceptance hinges on issuer credibility, reserve backing, and local rules (e.g., MiCA stablecoins in the EU).

3) Where do stablecoins shine vs CBDCs?

Stablecoins are strong in cross-border payments and remittances because they move 24/7 on open rails and plug into crypto platforms easily. They can reach users fast, even where banking access is patchy. CBDCs can match this over time, particularly as wholesale CBDC projects link national systems.

4) How do privacy and surveillance concerns compare?

CBDC privacy is a policy choice: many designs propose “managed anonymity” for small transactions with traceability above thresholds, raising debates about financial surveillance. Stablecoins can feel less state-visible, but they aren’t anonymous – issuers and platforms implement KYC/AML and sanctions screening.

5) What real programs should I watch?

Key references include China’s e-CNY, the digital euro process at the ECB, and U.S. debates around a US digital dollar / Fed CBDC. On the private side, watch how MiCA stablecoins roll out in Europe and how global card networks and fintechs route stablecoins into everyday checkout flows.

6) Will CBDCs replace stablecoins – or will they coexist?

Expect coexistence in the short-term. CBDCs likely lead domestic, retail use where monetary sovereignty, legal tender, and compliance are priorities. Stablecoins continue in open, cross-platform use (especially cross-border), provided regulation clarifies redemption, reserves, and payment rails. In the long term, expect CBDC dominance.