When we think of loans, banks are usually the first thing that comes to mind — the traditional intermediaries connecting those who need financing with those who can provide it. However, the digital transformation of finance has made it possible for borrowers and lenders to connect directly through P2P platforms, where technology replaces intermediaries and makes the process faster and more transparent.

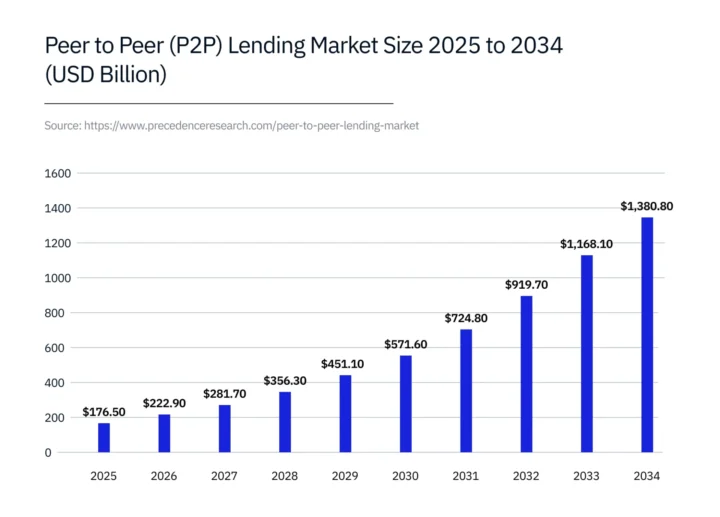

The rise of the FinTech industry has turned P2P lending into a major component of the alternative finance sector. According to Industry Research, more than 9,400 P2P lending platforms are operating in 75 countries, serving over 126 million users as of 2025. The global P2P lending market is valued at $176.5 billion, with growth projected to reach $222.9 billion in 2026 and $1.38 trillion by 2034.

Let’s take a closer look at how P2P lending works, who participates in it, and why it’s becoming a key element of the modern digital financial ecosystem.

What Is Peer-to-Peer Lending?

Peer-to-peer, or P2P, lending is a system that allows individuals or businesses to borrow and lend money directly to one another through specialized online platforms. These services handle the organizational and technical aspects of the process, including:

- Verifying borrowers

- Calculating credit ratings

- Automating payments

- Managing loan agreements

However, P2P platforms do not issue loans in their own name or use their own capital — all transactions take place directly between users.

The core idea behind the P2P model is to eliminate traditional intermediaries. In the conventional banking system, a bank accepts deposits and issues loans, earning from the difference between lending and deposit rates. In the P2P model, investors finance borrowers directly, earning interest income, while borrowers gain access to credit with lower fees and more flexible terms.

This model became possible thanks to the rapid development of FinTech infrastructure, digital identity technologies, and credit-scoring algorithms. Although loan decisions are largely automated and executed on the platform, the process itself is less centralized — risk assessment and funding are distributed among many private investors.

How Peer-to-Peer Lending Platforms Work

An online platform is the core element of any P2P lending system. It connects borrowers seeking flexible financing with investors looking for higher returns than traditional bank deposits can offer.

The interaction process typically follows several key stages:

- Registration and verification. Both borrowers and investors go through identity verification and provide financial information. The platform uses credit-scoring algorithms to assess creditworthiness and assign a risk rating to each borrower.

- Loan listing and funding. After verification, the borrower sends a loan request specifying the amount, term, and desired interest rate. Investors review available listings and select those that align with their strategy and risk tolerance. Often, a single loan is funded by multiple investors, allowing for risk diversification.

- Agreement and fund disbursement. Once a loan is fully funded, the platform generates an electronic agreement between the parties and transfers the funds to the borrower.

- Repayment and distribution. The borrower repays the loan according to the agreed schedule, while the platform automatically distributes the payments among investors, deducting a servicing fee.

This structure makes the lending process transparent and manageable. The platform provides the technological infrastructure, oversees cash flow, and ensures data security, allowing participants to focus solely on their financial goals, whether raising capital or earning income.

Importantly, the platform itself does not issue loans; its role is to organize and facilitate the process. As a result, it does not bear credit risk but assumes operational, legal, and reputational risks associated with its activities.

The model described above represents the classic form of peer-to-peer lending. In practice, however, platform operations can vary. Some P2P services work with intermediaries or partner institutions to handle legal documentation, while others maintain reserve funds to partially reimburse investors in the event of borrower defaults.

There are also hybrid models that involve not only individuals but also small businesses and institutional investors. In addition, new solutions are emerging, such as the issuance of securitized or tokenized assets, and the rise of decentralized finance (DeFi) protocols offering on-chain credit mechanisms.

Models of Peer-to-Peer Lending

While the core principles of lending platforms are similar, in practice, there are several models of P2P lending. They differ in how actively the platform participates in the process, how risks are distributed, and how transactions are structured.

The Classic (Direct) Model

This model is based on direct interaction between the borrower and the investor. The platform acts as a facilitator, providing the technological infrastructure but not intervening in the loan agreement itself. All terms — including amount, duration, and interest rate — are negotiated directly between the parties. This approach offers maximum transparency but requires a high level of trust and careful risk assessment from investors.

The Pooled (Collective) Model

In this case, investors’ funds are combined into a single pool from which loans are issued to various borrowers. Returns are distributed proportionally to each investor’s contribution. This structure helps mitigate individual risk and makes participation more accessible to retail investors, though it offers less flexibility in choosing specific borrowers.

The Automated Model

Modern platforms increasingly rely on algorithms and artificial intelligence (AI) to match investors with borrowers. Investors set parameters such as risk level, term, and desired return, and the system automatically allocates capital across suitable loans. This lowers the entry barrier and makes investing almost entirely passive, turning P2P lending into a managed investment tool.

In many cases, platforms combine these approaches, allowing users to choose between manual and automated investment modes. Such hybrid structures appeal both to experienced investors seeking portfolio control and to newcomers who prioritize convenience and diversification.

Advantages and Risks of Peer-to-Peer Lending

P2P lending has become one of the most prominent forms of alternative finance, combining technology, flexibility, and accessibility. Yet, like any investment tool, it offers not only opportunities but also certain risks for both borrowers and investors.

Advantages for borrowers:

- Accessibility. Borrowers can obtain financing without complicated bank procedures or collateral requirements. For many with limited credit histories, this may be the only viable way to secure funds.

- Flexible terms. P2P platforms often provide personalized interest rates and repayment schedules, allowing loans to be tailored to specific needs and goals.

- Speed. Loan approval decisions are made within minutes or hours — and in some cases, days — rather than weeks as in traditional banks.

Advantages for investors:

- Higher returns. Interest rates on P2P loans are generally higher than those offered by bank deposits or bonds.

- Portfolio diversification. Investors can spread their capital across numerous small loans, reducing overall exposure to individual defaults.

- Transparency. Platforms give investors access to borrower information and enable them to build personalized investment strategies.

Key risks of P2P lending:

- Credit risk. Borrowers may default on their loans, and platforms do not always compensate for resulting losses.

- Regulatory uncertainty. Legal frameworks for P2P lending vary across countries, affecting the level of protection for both investors and borrowers.

- Operational risk. Platforms can face technical failures, cyberattacks, or financial difficulties that disrupt their operations.

- Liquidity risk. P2P loans are often illiquid — withdrawing investments can be difficult, especially where secondary markets are underdeveloped.

In summary, P2P lending attracts participants with its mix of innovation and yield potential, but it also requires thoughtful risk management. For investors, it is a high-yield tool that comes with proportional responsibility; for borrowers, it serves as a faster and more flexible alternative to traditional bank loans.

Emerging Technologies and the Peer-to-Peer Lending Market

Modern P2P lending is evolving as a symbiosis of innovative financial technologies. The digitalization of processes, along with the integration of artificial intelligence (AI) and blockchain, is reshaping the very logic of lending, making it faster, more transparent, and more secure.

Artificial Intelligence and Big Data

Machine learning algorithms have become the primary tool for assessing creditworthiness. In addition to traditional banking criteria such as income level and credit history, platforms now analyze hundreds of variables, including:

- Behavioral data

- Online activity

- Transaction history

- Reputation metrics

This approach enables more accurate risk assessment, individualized interest rates, and lower default rates. AI technologies also help automate decision-making, minimize human error, and significantly speed up loan approvals.

Blockchain and Smart Contracts

Distributed ledger technology (DLT) has become the foundation for transparency and trust in decentralized P2P models. Smart contracts make it possible to execute agreements whose terms are written directly into code and enforced automatically — without intermediaries.

Each transaction is recorded on a distributed ledger, preventing data tampering and ensuring that payment histories remain fully auditable. Based on blockchain infrastructure, some platforms issue tokenized credit assets, creating secondary markets and improving investment liquidity.

According to a report by CoinLaw, approximately 30–40% of FinTech lenders plan to adopt blockchain solutions by 2025 to support loan verification and smart contract execution.

Integration with Decentralized Finance

One of the latest trends shaping the industry is the convergence between P2P lending and decentralized finance (DeFi) protocols. These systems allow cryptocurrencies to be used as payment instruments or collateral for loans, creating hybrid models in which investors earn returns in digital assets, while borrowers access capital outside the traditional financial system.

Integration with DeFi enhances the flexibility and global accessibility of P2P platforms, laying the foundation for a new decentralized credit architecture — one driven by smart contracts, tokenization, and algorithmic risk management.

According to DefiLlama, as of November 13, 2025, the total value locked (TVL) across DeFi lending protocols exceeds $70.8 billion.

Technological progress is transforming P2P lending from a niche innovation into a fully integrated component of the global financial system. The incorporation of artificial intelligence, blockchain, and decentralized solutions increases efficiency, reduces risk, and makes the market more open to private investors.