“Web3 is about user ownership.” That promise defined an entire generation of projects: from DAOs and Layer 1s to NFT platforms and decentralized social networks. But by 2025, it’s clear: ownership in Web3 is far more complex than wallet addresses and token drops.

Behind the headlines and governance snapshots, power continues to concentrate in three key domains:

- Token ownership — who holds the supply, and how concentrated are early-stage cap tables?

- Protocol-level control — who governs the code, the smart contracts, the multisigs, and the core infrastructure?

- Narrative shaping — who controls the messaging, media reach, and framing that influence how we perceive decentralization?

This article breaks down the real mechanics of ownership in Web3 as it stands in 2025, beyond whitepapers and Discord polls.

Whether you’re building, investing, or voting, understanding these hidden layers is key to knowing who actually owns what in the decentralized world.

Token Ownership: Cap Tables in Crypto Clothing

Tokens broaden access compared with Web2 equity, but most launches still favor insiders. Messari’s widely cited breakdown of Solana’s initial allocation shows roughly half went to insiders (team, company, and VCs), with only a sliver sold publicly, an emblem of how many L1/L2 ecosystems began life.

That dynamic feeds a long-running critique from Jack Dorsey: “You don’t own ‘Web3.’ The VCs and their LPs do.” Whatever one thinks of the rhetoric, the distribution facts that sparked the debate remain relevant when assessing who can swing governance or liquidity today.

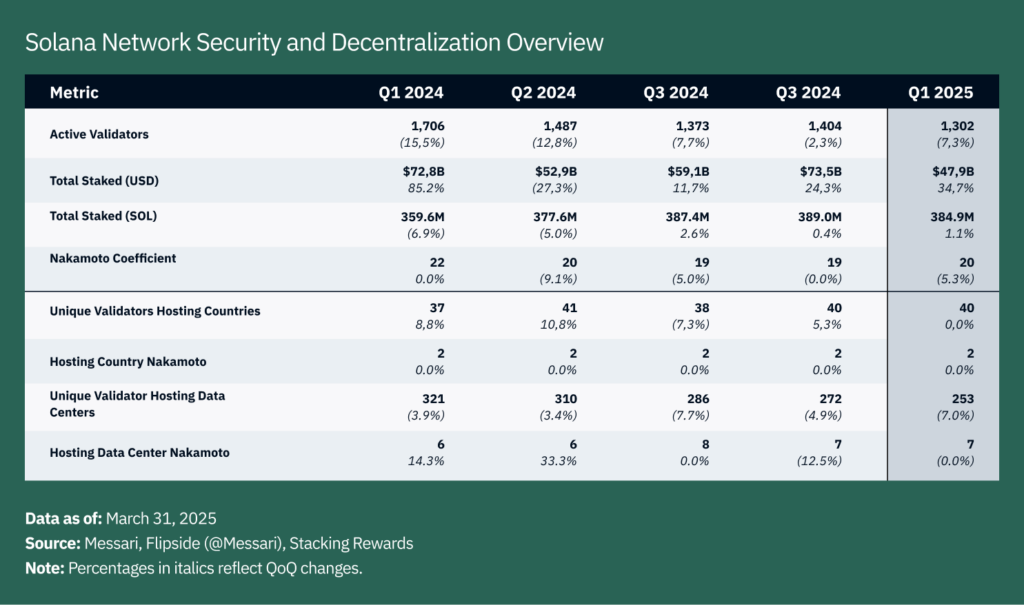

Ownership concentration is as much about genesis allocations as it is about where supply sits now. On Ethereum, the post-Merge era shifted influence toward large staking providers, while on Solana, a majority of circulating SOL is staked, magnifying validator and liquid-staking voting blocs.

Not all “ownership” is the same, either. Stablecoin issuers and many token contracts retain admin permissions. Tether says it has frozen more than $2.5-$2.9 billion in USDT linked to illicit activity to date; Circle’s USDC terms explicitly allow blocklisting. The feature helps law enforcement but underscores that holders rely on centralized discretion.

In short, it’s important to look at:

- Initial allocations and unlocks

- Treasury and foundation reserves

- Issuer controls (pause/blacklist functions)

- Concentration among exchanges, custodians, and staking pools

Protocol Power: Who Can Change the Rules, Pause the System, or Order the Blocks

Governance Reality vs. DAO Theater

Token voting exists, but turnout is often thin, and whales matter. In 2023, a16z used 15 million UNI to vote against a Uniswap deployment plan (enough at one point to tilt the tally, with only around 3% of the supply participating). The proposal still passed, yet the episode showed how a single actor can dominate a low-turnout vote.

Foundations and “Ratification” Votes

Also in 2023, the Arbitrum Foundation framed a major budget as a ratification after it had already begun moving funds (750 million ARB), prompting backlash and a redo. It was a reminder that early-stage governance often starts centralized, with community control increasing only after public pressure.

Admin Keys and Emergency Powers

Many DeFi protocols retain upgraders, guardians, or pause switches held by a multisig or foundation. These can save a platform during exploits, but consolidate power in a small committee by design. (If a protocol can be paused or upgraded by a handful of signers, governance is, at minimum, shared with them.)

Sequencers and Validators

Most high-throughput activity now lives on Ethereum L2s, which launched with single, centralized sequencers run by the core teams. Both Optimism and Arbitrum seem to be on a path to decentralize, and community proposals target 2025 milestones, but until those models land in production, ordering power remains concentrated.

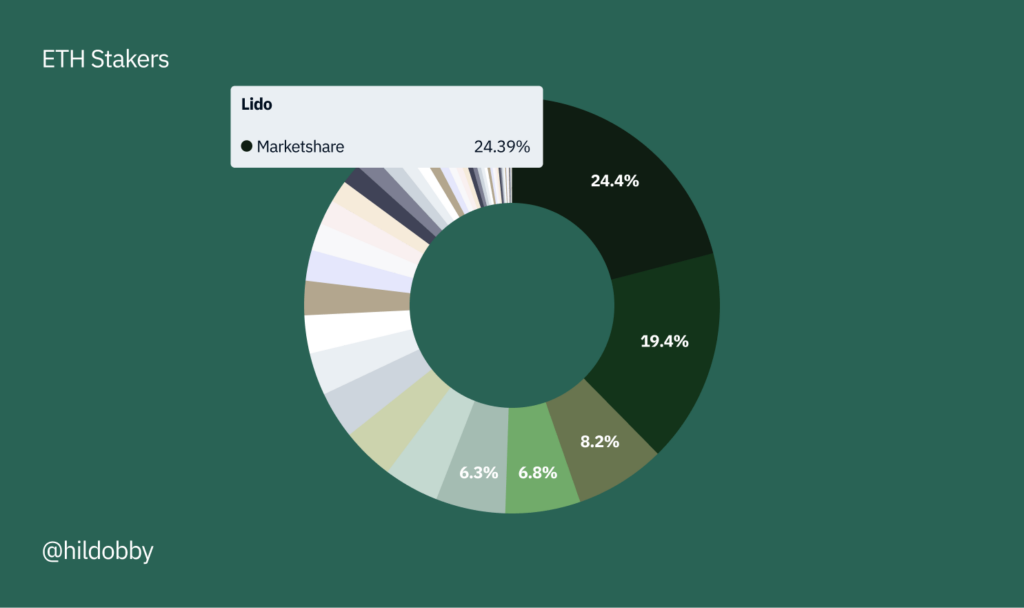

On the Ethereum mainnet, liquid-staking power is the headline risk. Lido’s share (once above 30%) has fallen into the mid-20s in mid-2025. That’s a healthier direction, but one provider still commands roughly a quarter of staked ETH, enough to anchor governance debates about caps and client diversity.

Infrastructure Chokepoints

Much “decentralized” usage is mediated by RPC providers and web frontends. Infura’s 2020 outage, which briefly disrupted wallets and exchanges, became a case study in how reliance on a few gateways can hobble dapps even when the chain keeps ticking. The pattern persists across providers and L2s.

Remember to check:

- Who signs upgrades

- Emergency powers and timelocks

- Sequencer/validator concentration

- Client diversity

- Dependency on single RPCs and web hosts

- Whether governance changes require on-chain execution or off-chain discretion

Narrative Control: Who Frames the Story (and the Policy)

VCs and Advocacy

Big investors fund protocols, but they also publish research, host podcasts, and lobby. a16z’s State of Crypto reports, policy posts, and Washington presence shape agendas from stablecoin bills to DeFi “safe harbor” concepts now being floated to the SEC. Whether one sees this as necessary movement-building or soft capture, it undeniably steers discourse and rulemaking.

Personalities and Platforms

Web3 runs on social media: a handful of founders, influencers, and fund executives can set narratives (and, sometimes, prices) in a single thread. Dorsey’s 2021 broadside still frames ownership debates; pro-crypto and skeptical media cycle those frames back into policy conversations.

Regulatory Theater

Stablecoins illustrate the narrative paradox. Proponents pitch them as the internet’s cash layer; critics point to blacklist powers and offshore governance. Law-enforcement freezes (in the billions) now feature in both sides’ talking points, either as proof of responsible controls or proof of centralization.

Make sure to check:

- Who funds the reports you’re reading

- Who’s paying for policy shops and coalitions

- Which outlets and conferences amplify specific talking points

- How much “community” comms flows through foundation-owned channels

A Quick Field Guide to “Who Owns What”

When evaluating any Web3 project:

- Follow the allocations. Map insiders vs. community, vesting schedules, and anticipated unlocks; look for public sale share relative to private rounds. High insider share tends to correlate with weaker performance and weaker governance legitimacy.

- Trace the keys. Identify upgrade roles, guardians, and kill-switches; require timelocks and on-chain votes for major changes.

- Grade the operators. For L1s: validator and client diversity; for L2s: sequencer decentralization plan and who runs bridges. Beware single-entity order flow or bridge control.

- Interrogate the stack. Which RPC, hosting, and analytics services sit between users and contracts? Is there a fallback to multiple providers or a local node?

- Contextualize the comms. Read policy posts and “state of” reports with their incentives in mind. Advocacy can be valuable; it’s also directional.

The Bottom Line

Web3 has expanded the circle of ownership. Airdrops and permissionless markets let millions hold pieces of networks they use.

However, meaningful control still bunches up around early investors and foundations, large staking pools and sequencers, and well-funded advocates who set the story arc.

The task for 2025-26 is turning “progressive decentralization” from a slide into shipped governance: capped concentrations, diversified clients, decentralized sequencing, real timelocks, and credible community budgets.

Until then, user-ownership is real but partial. To see who really owns what, follow three threads (the cap table, the keys, and the comms) and assume power sits where those threads intersect.