- 1/8 CryptoProcessing by Coinspaid: What “Crypto Acquiring” Looks Like When You Treat It Like Payments Infrastructure

- 2/8

- 3/8

- 4/8

- 5/8

- 6/8

- 7/8

- 8/8

Accepting a crypto payment is only one part of the payment lifecycle. Once a transaction has been completed, businesses may need to address settlement, reconciliation, reporting, compliance, and customer support. Questions can arise when payments are sent on the wrong blockchain network, invoices are paid through multiple transactions, or settlement timing differs from internal financial processes.

To address these operational requirements, crypto payment infrastructure has evolved beyond simple payment acceptance. Crypto processing typically combines payment acceptance, transaction confirmation, settlement, reporting, and related operational functions within a single workflow. CryptoProcessing by Coinspaid is one example of this type of infrastructure.

At a glance

- Customers can pay in 20+ leading cryptocurrencies and stablecoins

- Settle in crypto or convert and withdraw via fiat path

- API-led implementation with payment-status callbacks and merchant flows

- Pay-ins (checkout/invoices) and payouts/withdrawals, depending on setup

Why Crypto Payments Are Still Hard

In CryptoProcessing’s own positioning, the fundamentals are straightforward: existing merchants can accept payments in a broad set of popular cryptocurrencies, convert incoming funds into traditional currencies quickly to reduce volatility exposure, and settle proceeds through a fiat path when the business needs that predictable “bank account outcome.” The point is that crypto becomes manageable.

At the same time, if you ask merchants why “accepting crypto” hasn’t become as routine as adding a new card processor, the answers are rarely philosophical and more operational.

The infrastructure tends to be fragmented. In many setups, a payment button is one provider, the wallet layer is another, the conversion step happens elsewhere, and fiat settlement depends on yet another vendor relationship. Each seam adds new failure modes: inconsistent transaction identifiers, mismatched reporting formats, different compliance expectations, and support teams bouncing issues between vendors.

Igor Skirnevskii, CPO at CryptoProcessing, sees the same hesitation from people who are already interested in the channel. “Most users are interested in crypto already,” he says, “but they still worry about volatility, compliance, and whether the integration will create operational headaches for their teams.”

Those concerns usually fall into four buckets:

- Volatility, as merchants don’t want revenue to behave like a trading account. If the value moves between the moment the customer pays and the moment the business settles, margins become unpredictable.

- Compliance, which arises once crypto becomes meaningful revenue; merchants need to demonstrate KYB/KYC discipline, AML controls, and monitoring. “We accept crypto” becomes a governance statement.

- Integration, as crypto payments need familiar states — pending, confirmed, failed — along with reliable callbacks and logic that can handle partial payments or expirations without manual intervention.

- Fiat settlement, as most businesses still pay suppliers and taxes in fiat, so even when customers pay in crypto, settlement and reporting need to land in the currencies their operations run on.

There is also a customer-facing layer to the problem. “Another big concern is customer experience,” Skirnevskii adds. “If checkout feels complicated, conversion drops immediately.”

That is why CryptoProcessing’s bet is not that merchants need “more crypto,” but that they need fewer moving parts and clearer rules. As Skirnevskii puts it, the goal is to give merchants “a familiar payment infrastructure: instant conversion, strong compliance coverage, simple integrations, and a checkout flow optimized for high payment completion rates.” In other words, the product thesis is to make crypto feel predictable enough to operate.

What “Crypto Processing” Actually Means, And Why It’s Not Just A Crypto Checkout Button

In a traditional PSP model, everyone understands the broad shape of the payment lifecycle: authorization, capture, settlement, and disputes. Crypto changes the rails, which changes the lifecycle.

Crypto processing solutions are an attempt to standardize that lifecycle for merchants. In its simplest form, it’s a flow that looks like: accept crypto → confirm the transaction → convert/settle → reconcile/report. But the real work is translating blockchain realities into merchant-friendly states.

A merchant doesn’t want to explain to a customer that the payment is “in the mempool.” They want a clean set of statuses that map to business actions: do we deliver the goods, do we wait, do we issue a refund, do we mark it failed, and do we ask the customer to try again? This is where crypto processing differs most from a “crypto checkout button.” It’s not about showing crypto as an option but rather about making it behave like a payments infrastructure.

The differences from card PSPs are consequential:

- Settlement logic is confirmation-driven. Cards settle through networks and cycles; crypto settles through blockchain transaction state and confirmation logic.

- Dispute dynamics change. On-chain transfers don’t come with classic card chargebacks. That reduces one kind of cost, while pushing more responsibility onto fraud prevention, refund policy discipline, and monitoring.

- Conversion becomes a control surface. In card payments, settlement cycles are part of the deal. In crypto payments, merchants often want conversion now because the business didn’t sign up to run a mini trading desk.

CryptoProcessing Ecosystem: Not a Single Tool, But a Connected Set of Components

CryptoProcessing frames itself as an ecosystem rather than a single tool, and that’s not just marketing semantics. Merchants need to know what happens around acceptance, which is possible to achieve with:

- Merchant gateway: the acceptance layer that powers pay-in flows (checkout, invoices, payment forms) and turns blockchain payment activity into merchant-ready statuses.

- Business wallet layer: a business environment for balances and treasury operations, which is not a consumer wallet, but something that fits operational finance workflows.

- Exchange functionality: embedded conversion that supports instant crypto-to-fiat and other exchange actions so volatility exposure can be minimized by design, not handled manually.

- Fiat settlement infrastructure: the bridge to the “real world” for businesses that need proceeds in bank-account terms, with settlement schedules and withdrawals integrated into the operating model.

- OTC (where relevant): for larger-volume needs, some merchants care less about “spot conversion” and more about execution quality and bespoke settlement. If CryptoProcessing positions OTC for your target audience in owned materials, this is where it belongs, as an enterprise liquidity option.

What CryptoProcessing Does In Practice

If you want to understand whether a crypto payments provider is built for real businesses, don’t start with the list of supported assets. Start with what happens when things go slightly wrong because in payments, they always do.

Customers don’t always pay in one clean transaction. Sometimes they pay in two transfers. Sometimes they send the right amount after the invoice window has expired. Sometimes they initiate a payment, close the tab, and come back later asking whether the merchant received it. Sometimes they pay from a wallet that makes manual entry error-prone, especially on mobile, and the merchant ends up with a support ticket that begins with “I sent it, but…”

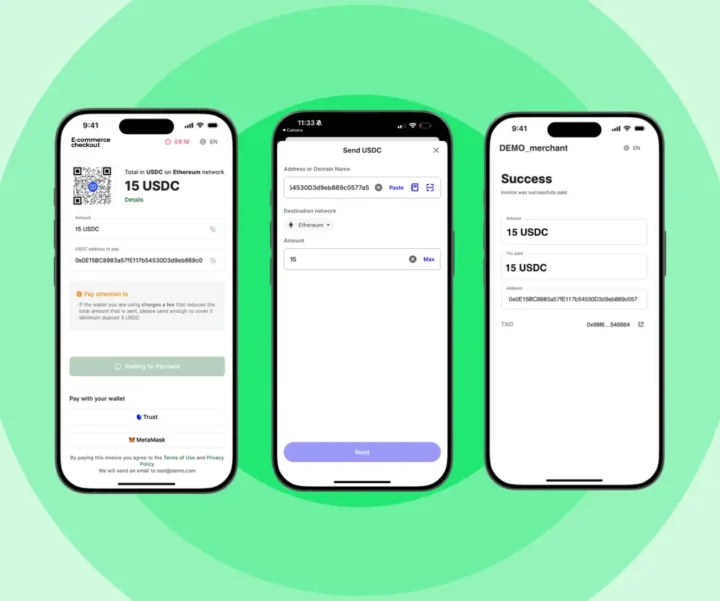

CryptoProcessing has been using product updates to target those specific failure modes. A good example is Pay with Wallet, introduced for invoice payment forms to reduce manual-entry friction for users paying with wallets like MetaMask and Trust Wallet.

For Igor Skirnevskii, CPO at CryptoProcessing, that customer layer is often the first place merchants see value. “In most cases, the first visible impact is access to new customers,” he says. “Crypto users are global, highly active online, and often prefer paying with digital assets over traditional banking methods.”

On the infrastructure side, network support matters for the same reason. When fees rise or confirmation times vary, merchants feel it in conversion rates and customer support volume. CoinsPaid Media’s updates about expanding EVM network support, including integrations such as Polygon and Layer-2 networks, fit into a broader merchant reality: “cheaper and faster rails” aren’t a crypto talking point but a payments performance variable.

Skirnevskii points to the same second-order effect: once merchants get past the initial demand signal, they start paying attention to the operating model behind it. “After that, merchants usually start appreciating the operational benefits as well,” he adds, “especially faster settlements and lower processing costs compared to some traditional cross-border payment methods.”

Stablecoin expansion plays a similar role: for merchants who care about predictable value, the choice of settlement assets and rails is part of the product, not an accessory. The theme across these details is consistency: crypto processing becomes valuable when it turns a variable system — different wallets, networks, confirmation behavior, and user habits — into predictable merchant outcomes.

What Existing Merchant Implementations Show

Viewed together, CryptoProcessing’s published case studies are less about promoting crypto payments than about illustrating how crypto payment infrastructure functions in different operational environments. Although each example reflects the experience of a single merchant, they highlight recurring themes around payment costs, customer behaviour, reconciliation, and settlement.

Payment costs

One published case study involving Mirai Flights reports lower payment processing fees following the introduction of crypto payments, alongside broader business growth during the same period. While these figures relate to a specific implementation and cannot be generalized, they illustrate how payment costs may differ depending on payment methods, transaction corridors, and the underlying payment infrastructure.

Customer payment behaviour

A case study involving Frog reports a higher average order value for transactions completed with crypto than for those completed through traditional payment methods. The figures do not establish that the payment method itself caused the difference, as customer mix, purchasing behaviour, and product type may also influence the outcome. They do, however, illustrate that payment preferences can vary across customer segments.

Operational processes

The Transformify case study focuses primarily on finance operations rather than payment acceptance itself. It reports improvements in areas such as reconciliation, reporting, and chargeback handling. While the reported figures are specific to that implementation, the example highlights the operational considerations that often accompany crypto payment processing after a transaction has been completed.

Payment mix

A published case study involving AdsKeeper reports that a share of customer payments was completed using digital assets. Although the results relate to a single merchant environment, they illustrate how crypto payments can become one component of a broader payment mix in some business models.

Taken together, these examples emphasize that the operational aspects of crypto payments extend beyond payment acceptance. Settlement, reconciliation, reporting, treasury management, and customer support all become part of the payment lifecycle, and the way these processes are managed depends on the requirements of each merchant implementation.

Where It Fits Best: Industries That Need Global Reach and Operational Discipline

Crypto processing solutions are the most naturally aligned with sectors that are digital by default, global in customer base, and sensitive to friction in checkout and settlement.

- E-commerce is an obvious fit when crypto audiences overlap with the merchant’s customers, and when the checkout experience can be improved rather than complicated.

- SaaS and digital services care about predictability: settlement outcomes that reconcile cleanly and don’t introduce a new layer of customer support debt.

- Marketplaces live and die by payout complexity; when there are many parties on both sides of a transaction, structured pay-in and payout workflows become crucial.

- Fintech-adjacent platforms care about compliance posture and operational controls because they inherit scrutiny from partners and regulators.

Across these categories, the common denominator is not so-called “crypto enthusiasm” but the need for payment flows that feel simple to customers and controlled for merchants. “A good crypto checkout experience should feel as simple and reliable as any traditional online payment,” says Yurii Zaitsev, Head of Product Department at CryptoProcessing. “The process needs to be intuitive, fast, and transparent, with clear payment instructions, accurate exchange rates, predictable settlement times, and minimal steps required to complete a transaction.”

That is especially important for mainstream digital businesses. If a customer has to manually check rates, copy wallet addresses, second-guess settlement timing, or wonder whether funds were received, crypto stops feeling like a payment method and starts feeling like a task.

“Customers should not need to understand the technical complexity of blockchain networks to successfully make a payment,” Zaitsev adds. “The best checkout experiences remove friction, reduce the risk of payment errors, and provide confidence that funds have been received and processed correctly.”

For merchants, the same logic extends behind the scenes. Zaitsev says CryptoProcessing focuses on “simplifying every stage of the payment journey,” including support for multiple cryptocurrencies and wallets, real-time exchange rates, automated reconciliation, payment status visibility, and infrastructure resilience.

Bank-underserved industries do exist in the crypto payments universe, but they don’t need to be the center of this story. The broader point is that crypto processing is becoming a tool for businesses that want global payment optionality and want it without operational chaos.

FAQ

This is one of the most common crypto payment mistakes. For example, a customer may intend to pay USDT but choose the wrong blockchain network in their wallet. Whether the funds can be recovered depends on the asset, network, address type, and the processor’s ability to detect or access the transaction. Merchants shouldn’t promise automatic recovery. The safest approach is to make the checkout page extremely clear: show the exact currency, network, amount, wallet address, and payment window, and instruct customers not to manually change the network in their wallet.

Yes, this is one of the main reasons businesses use crypto processing rather than a simple wallet setup. A merchant can allow customers to pay in crypto while choosing to convert incoming funds into fiat or stablecoins, depending on the available settlement options and account setup. This matters for accounting, treasury, and volatility management: the merchant can serve crypto-paying customers without necessarily treating crypto as an investment asset.

Crypto refunds need a clear policy because blockchain payments don’t reverse like card payments. In most cases, a refund is a new outgoing transaction rather than a cancellation of the original one. Merchants should decide in advance which currency they will refund in, how they will calculate the refund amount if exchange rates change, who pays network fees, and what information the customer must provide. For customer experience, this should be explained before checkout or in the refund policy — not improvised after a support ticket arrives.

They can if the setup is manual. The accounting challenge is not only “crypto in, fiat out,” but matching each payment to an order, exchange rate, fee, settlement currency, and payout record. A proper crypto processing setup reduces that workload by using payment IDs, statuses, reports, and reconciliation data that finance teams can connect to their normal processes. Merchants should still involve accounting early, especially if they operate across multiple currencies or settle partly in crypto.

The timeline depends less on the code itself and more on readiness: onboarding, KYB, integration route, settlement preferences, and internal approvals. A plugin-based setup can be faster for standard e-commerce flows, while API integration takes longer when the merchant needs custom checkout, marketplace logic, payouts, or advanced reporting. The practical rule is to prepare the business flow first: which assets to accept, what settlement currency to use, who handles exceptions, and how finance will reconcile transactions.